Smart Ways to Pay Off Debt Faster Without Stress

Let's face it: debt can feel like a heavyweight, dragging you down and clouding your financial future. Whether it’s credit card balances, student loans, or a personal loan, tackling it aggressively often seems like the only way to break free. But what if you could accelerate your debt payoff without adding more stress to your already packed life? It’s not just possible; it’s about working smarter, not harder. This guide dives into practical, actionable strategies to help you conquer your debt faster and with a lot less anxiety.

Why It’s Crucial to Tackle Debt Aggressively (But Smartly)

High-interest debt is a silent killer of your wealth. Every dollar you pay in interest is a dollar that could have been invested, saved, or spent on something that truly brings you joy. Beyond the financial drain, the constant weight of debt can significantly impact your mental well-being, leading to stress, anxiety, and even relationship strain. By implementing smart strategies, you not only free up cash flow sooner but also gain invaluable peace of mind. It's about reclaiming control of your financial narrative.

Real-World Impact: Data Snapshot

Consider the average American carrying nearly $6,000 in credit card debt. At an average APR of around 20%, that’s potentially upwards of $1,200 in interest payments annually! Multiply that by years, and the numbers become staggering. A 2023 study by the Federal Reserve indicated that a significant portion of households struggle with debt payments, highlighting the pervasive nature of this financial challenge. However, individuals who successfully pay off high-interest debt typically report substantial improvements in their savings rate and overall financial confidence within 2-5 years of focused effort.

Mastering the Art: Smart Strategies for Faster Debt Payoff

Getting out of debt doesn't have to be a painful grind. It's about strategic moves and consistent action.

1. The Power of the Debt Snowball and Debt Avalanche

These are two popular, effective methods to organize your debt payoff. Choose the one that best suits your psychological makeup and financial situation.

- Debt Snowball: This method involves paying off your smallest debts first, regardless of interest rate, while making minimum payments on others. Once a small debt is paid off, you roll that payment amount into the next smallest debt. The psychological wins of quickly eliminating debts can be incredibly motivating.

- Debt Avalanche: Here, you prioritize paying off debts with the highest interest rates first, while making minimum payments on the rest. Mathematically, this saves you the most money on interest over time. It requires more discipline but yields greater financial rewards.

2. Negotiate Your Interest Rates

Don’t be afraid to pick up the phone and call your creditors, especially for credit cards. Explain your situation and your commitment to paying off the balance. Often, they’ll be willing to lower your interest rate, sometimes significantly, to keep your business. A lower APR means more of your payment goes towards the principal, slashing payoff time.

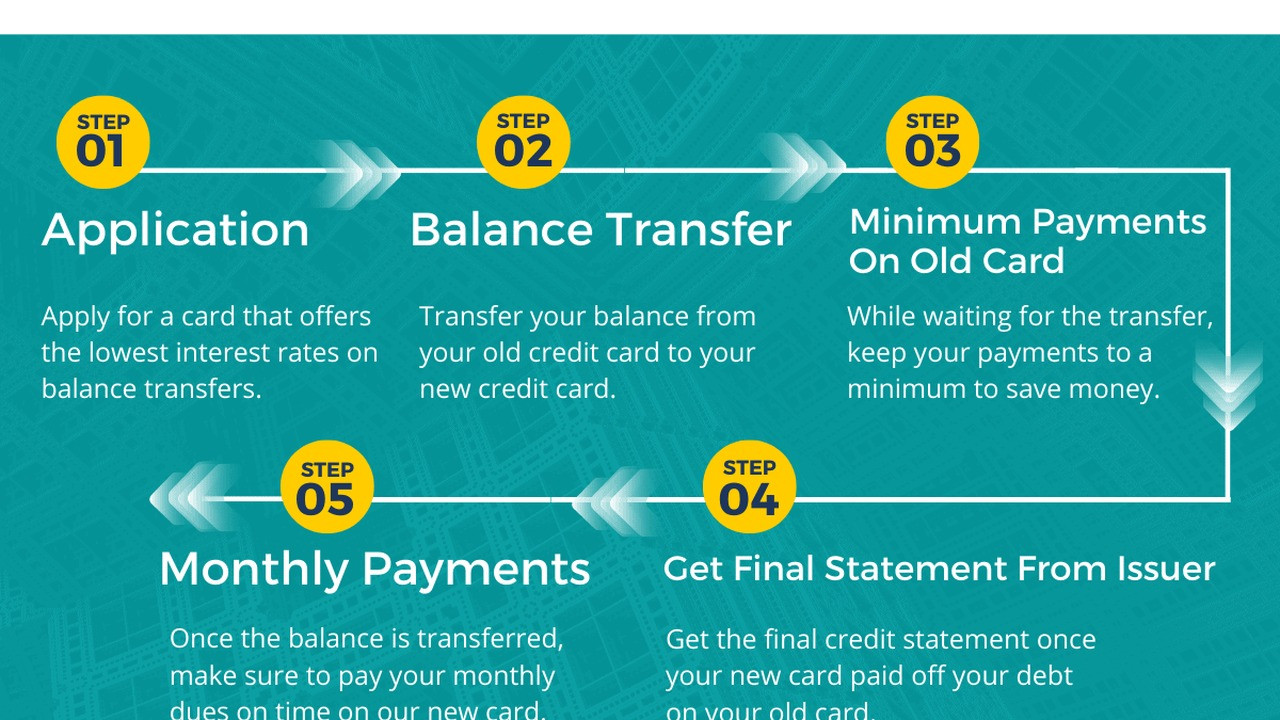

3. The Balance Transfer Tactic

For high-interest credit card debt, a balance transfer to a card with a 0% introductory APR can be a game-changer. Be aware of transfer fees (usually 3-5%), but if the intro period is long enough and you can pay off a substantial amount, the savings in interest can be immense. The key is to have a solid plan to pay off the balance before the intro period ends.

4. Boost Your Income, Boost Your Payoff Speed

Finding extra cash to put towards debt is crucial. This could involve:

- Taking on a side hustle (freelancing, delivery services, selling crafts).

- Asking for a raise or seeking a higher-paying job.

- Selling unused items around your house.

- Monetizing a hobby or skill.

Every extra dollar, after essential needs, can dramatically accelerate your journey.

5. Automate Your Payments and Extra Payments

Set up automatic minimum payments to avoid late fees, but also set up an automatic transfer of your "extra" debt payment directly from your checking account to your debt principal. Treat this extra payment like any other bill – non-negotiable. Automation removes the temptation to spend that money elsewhere.

6. The "Found Money" Strategy

Did you get a tax refund? A bonus at work? A gift? Instead of letting this money disappear into general spending, immediately allocate it to your debt. This "found money" can make a surprisingly big dent without feeling like a sacrifice from your regular budget.

Here’s a simple breakdown of how different payoff methods can impact your timeline:

| Debt Scenario | Minimum Payments Only (Est. Time) | Debt Avalanche (Est. Time) | Debt Snowball (Est. Time) |

|---|---|---|---|

| $10,000 Credit Card Debt @ 20% APR, $300/month payment | ~47 months | ~45 months (saves ~$1,500 interest) | ~48 months (builds momentum) |

| $20,000 Student Loan @ 6% APR, $500/month payment | ~44 months | ~43 months (saves ~$2,000 interest) | ~44 months |

*Note: These are simplified estimates and actual payoff times can vary based on exact payment allocation and potential interest rate changes.

Common Pitfalls to Sidestep

Even with the best intentions, there are a few common traps that can slow down your progress.

- Taking on New Debt: This is a cardinal sin. While trying to get out of debt, resist the urge to finance new purchases with credit cards or loans.

- Making Only Minimum Payments: This is the slowest path to debt freedom. If you can afford more, do it.

- Not Tracking Progress: Without seeing how far you've come, it's easy to get discouraged. Keep a visual tracker (a spreadsheet, an app, or even a printed chart) to stay motivated.

- Ignoring a Budget: A budget is your roadmap. Knowing where your money goes is essential for identifying areas where you can cut back and allocate more towards debt.

- Falling for "Get Rich Quick" Debt Schemes: Be wary of any program promising to erase debt magically. Stick to proven, ethical financial strategies.

Reclaim Your Financial Freedom Today

The journey to debt freedom is a marathon, not a sprint, but with smart strategies, you can definitely pick up the pace. Start by choosing a payoff method that resonates with you, whether it's the psychological wins of the snowball or the financial logic of the avalanche. Don't hesitate to negotiate with creditors, explore balance transfers wisely, and actively seek ways to boost your income. By automating your payments and being disciplined with "found money," you'll be amazed at how quickly you can shed that debt burden. Take that first smart step today—your future self will thank you.

FAQ

What is the difference between the debt snowball and debt avalanche method?

The debt snowball method focuses on paying off the smallest debts first, regardless of interest rate, offering psychological wins. The debt avalanche method prioritizes debts with the highest interest rates first, saving you the most money on interest over time. Both are effective, but they cater to different motivations.

How can I increase my income to pay off debt faster?

You can increase income by taking on a side hustle (like freelancing or delivery services), asking for a raise at your current job, switching to a higher-paying position, selling unused items, or monetizing a hobby. Even small amounts of extra income can make a big difference when strategically applied to debt.

Is a balance transfer a good idea for paying off debt?

A balance transfer can be an excellent strategy for high-interest credit card debt if you can secure a 0% introductory APR. It allows you to pay down the principal without accruing significant interest during the promotional period. However, be mindful of balance transfer fees and ensure you have a plan to pay off the balance before the introductory rate expires to avoid high standard APRs.

How often should I review my debt payoff progress?

It's beneficial to review your debt payoff progress at least once a month. This allows you to track your successes, celebrate milestones, and make any necessary adjustments to your budget or payment strategy. More frequent reviews (e.g., weekly) can also help maintain momentum and prevent financial drift.